96% of Californians Picked Just Four Health Plans Through Covered California. Are Small Plans Getting Squeezed Out?

by

Dan

Diamond,

California Healthline Contributing Editor

Wednesday, December 4, 2013 - California Healthline

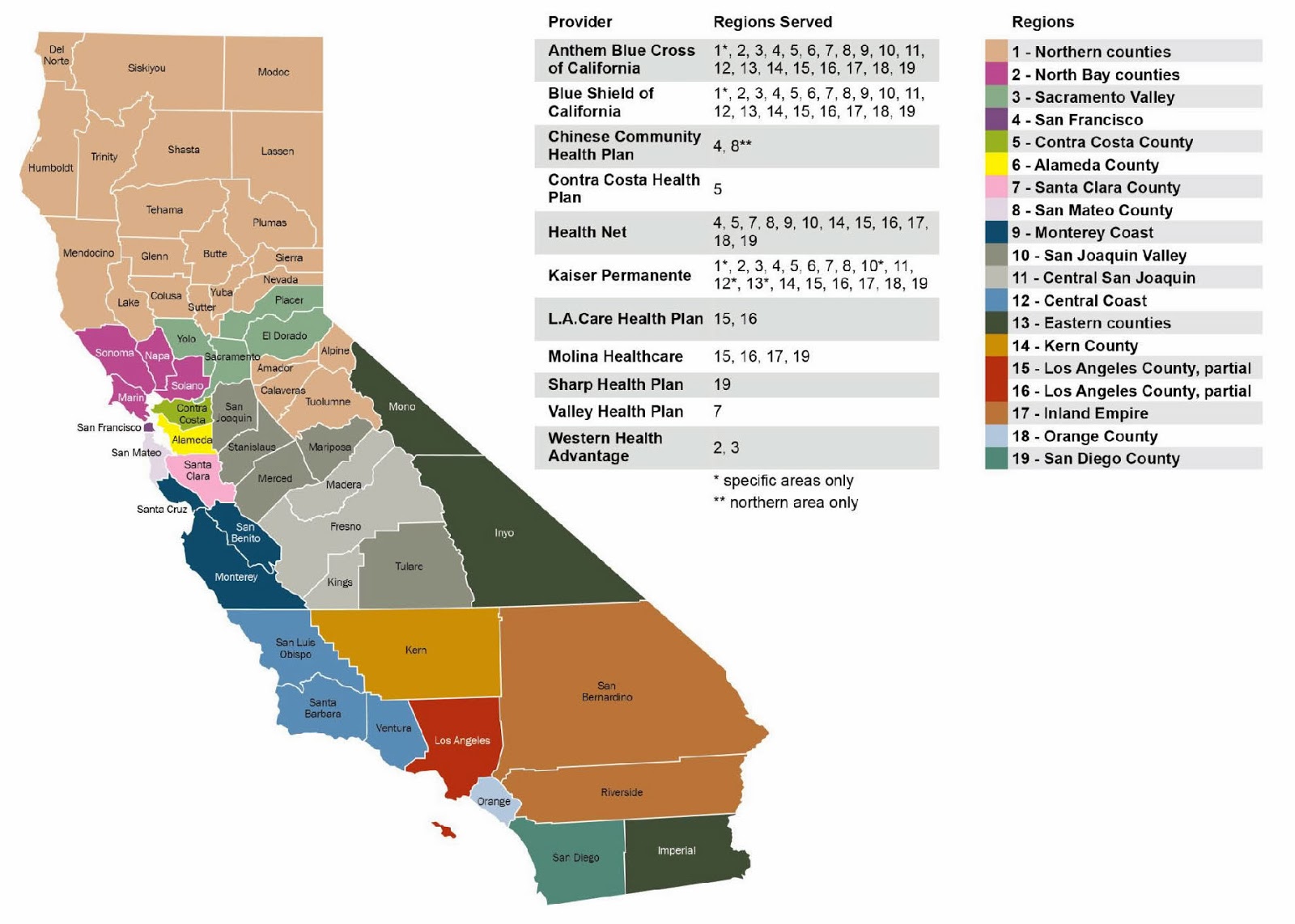

Anthem Blue Cross had 1,591 people use Covered California to get subsidies

and sign up for its health plans in October.

Valley Health Plan had five.

That data point's taken from a Covered California release that offers some of the first

insight into the makeup of early enrollees through the exchange and which plans

they're picking. And while it's hardly fair to directly compare the two issuers

-- Anthem has a presence in all 19 of Covered California's regions, whereas

Valley is only offering plans in Santa Clara County -- the contrast is

eye-catching.

It's also telling. The biggest players, so far, are getting enormous market

share from Covered California's customers. The smaller plans are seeing a

trickle.

So Far, Exchange Strengthens Market Position of Large Plans

The Affordable Care Act's insurance exchanges were supposed to open up the

market -- "more choices, greater competition," trumpets a 2010 White House fact sheet. They were a rare Obamacare idea

that's enjoyed consistent

Republican support. And several experts told "Road to Reform" in July that

Valley and other small health plans were the ones to watch in California's exchange.

But what if the exchanges are leading to market consolidation, not

competition? It seems premature to ask, but here's a picture of

the

Covered California market from October:

- 28% of customers picked Anthem plans;

- 26% picked Kaiser Permanente plans;

- 26% picked Blue Shield of California plans; and

- 16% picked Health Net plans.

That means that fewer than 4% of customers were divvied up between the other

seven plans currently available on the exchange.

It's worth repeating: Unlike smaller plans like Valley, Sharp and a few

others that only focused on a slice of California's population, the "big four"

issuers chose to offer plans

across the state. Their broader presence helped goose their enrollment

numbers.

But that alone can't explain customers' shopping patterns, because similar

proportions show up when drilling down into individual regions.

- In October, Valley captured about 2% of new Covered California customers

in Santa Clara County; the other 98% were split between the big four.

- Contra Costa Health Plan got about 4% of the new customers in its county;

the rest went with the big four.

- Western Health Advantage saw fewer than 2% of new customers in the North

Bay and Sacramento Valley regions, while the remainder were split between

Anthem, Kaiser and Blue Shield. (Health Net isn't offering plans in those

regions).

Three Drivers of Customer Behavior

So why the market dominance by the large issuers? Experts suggest a few

factors.

The power of name recognition: The big four plans presently command

more than 80% of the individual insurance market in California. "One might

expect [the large plans] to have an even bigger advantage early on due to their

recognized brands and marketing muscle," Kaiser Family Foundation's Larry Levitt

told California Healthline via email.

The power of being an ex-customer: Some new plan members are very

recent old members; officials at several plans suggested that more than

10% of new enrollees were former customers. So while most of the sign-ups may be

with the major plans like Anthem and Kaiser, most

of the plan cancellations have been with them, too.

Challenges with the website: The lack of plan quality ratings and provider directories may have

hindered head-to-head comparisons -- even as cautious insurers delayed their

marketing campaigns -- again leading customers to stick with names that may have

been familiar.

Meanwhile, price was expected to be a lever for consumer choice -- that was the case in Massachusetts, at least. But so far,

it's unclear whether it's being weighted as heavily in California. In several

regions, there didn't appear to be much correlation between plan prices and

sign-ups.

Still, it's "way too early to read too much into the early enrollment

numbers," Micah Weinberg of the Bay Area Council told "Road to Reform."

The October sign-ups weren't representative of Covered California's expected,

and eventual, pool of customers, Weinberg pointed out. Look at the huge

percentage of non-subsidized customers, who out-numbered subsidized customers by

about five-to-one, he noted. Or the lack of Spanish-speaking customers, who made

up just 3% of enrollees in October but represent 60% of the state's uninsured

population, Anna Gorman reports at Kaiser Health News.

"The population that's enrolled to date, as far as we understand, is a

population with greater health care needs," Weinberg added.

"So they may be more likely to go with what they know, or go with the sort of

well-known needs."

"But we'll know a lot more later on," Weinberg predicted.

Will Small Plans Stick it Out?

Weinberg and others also raise the question of whether more plans are

necessarily better for consumers. Some studies have suggested that just

three-to-four insurers are enough to make a region competitive, although

exchange rates significantly fall as the number of competitors rises.

Would the smaller plans drop out if they don't get enough customers? That's

unlikely, experts and historical evidence suggest.

"I suspect there is a volume level at which a plan would decide it's not

worth the administrative expense associated with participating," Kaiser's Levitt

muses, "but I imagine that's pretty low. Probably the bigger issue is in putting

together a provider network ... [with] a whole-new provider network, the

economics may not work at low volumes."

And exchanges can lead to disproportionate enrollment gains for their smaller

plans -- eventually. In Massachusetts, Neighborhood Health Plan saw its

enrollment nearly double

to about 230,000 between 2006 and 2011, largely attributable to the state's new

mandate and insurance exchange.

Meanwhile, Blue Cross Blue Shield of Massachusetts -- the state's largest

insurer by number of members -- saw the biggest

decline in market share across that period, losing about 175,000 enrollees

even as other plans added more than 500,000.

"Overall, the Health Connector has spurred competition and created an

efficient distribution model for smaller plans and new offerings," according to

David Williams, president of the Massachusetts-based Health Business Group. "And

new plans are [still] signing up," he added, noting that two more issuers are

joining the state's exchange in 2013 and 2014.

Signs of Success

There has been some attrition. Two smaller plans that were initially accepted

into Covered California -- Ventura

County and Alameda

Alliance -- ended up not participating in the exchange's first year.

But for at least one local insurer, there are signs of success.

The Chinese Community Health Plan, which is offering plans in the San

Francisco and San Mateo regions, had targeted 4,950 new members by the end of

March 2014 open enrollment, spokesperson YoungSoo Cho told California

Healthline. (The plan had a total of 15,363 members before Covered

California opened for business.)

In October, the plan signed up 216 customers through Covered California --

roughly 12% of all new enrollees in the two regions it serves -- using a

strategy that combines raising awareness, a targeted enrollment push, and five

in-person enrollment centers, Cho says.

And the pace is picking up; sign-ups for the Chinese Community Health Plan

nearly quadrupled in November.

"As of this week, we have exceeded the 1,000 new members through the exchange

and we are confident we will hit our goals" by the end of the open enrollment

period, Cho added.

© 1998 - 2013. All Rights Reserved. California

Healthline is published daily

for the California HealthCare

Foundation by The Advisory Board Company.

{kind=link}